You’ve heard the "all-in" stories.

The founder who bet his last dollar, slept on the office floor, and turned a garage startup into a multi-million dollar empire. We celebrate these stories. We treat "all-in" as a badge of honor.

But here is the truth nobody wants to tell you at the networking mixer: "All-in" is just another word for "unprotected."

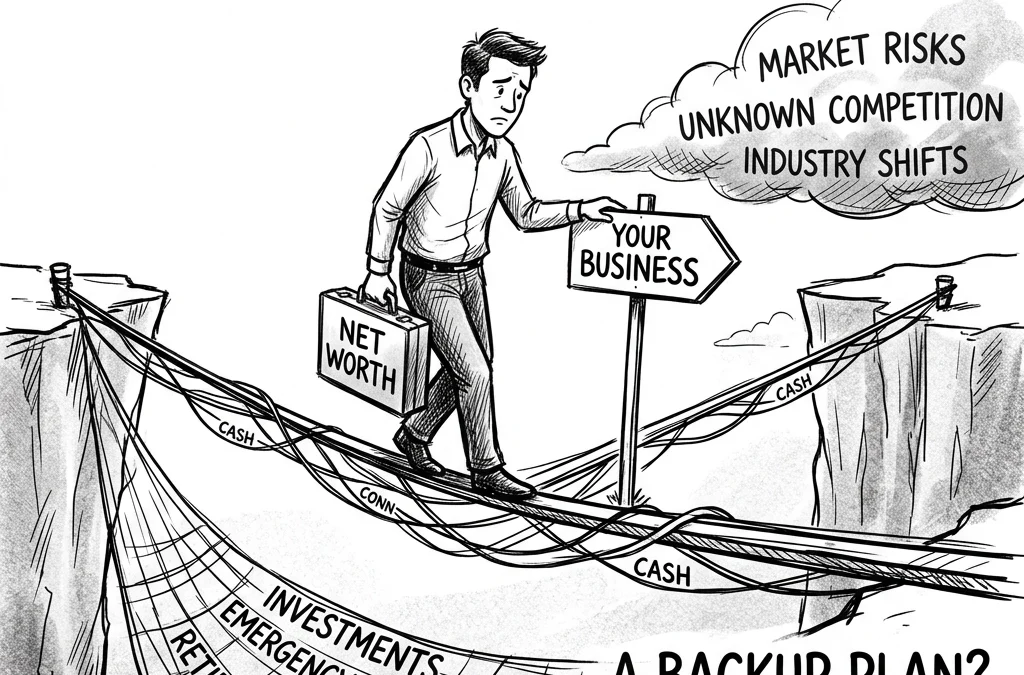

If you are like most business owners I work with, your business isn't just your job. It’s your identity. It’s your creative outlet. And, most dangerously, it is 80% to 90% of your total net worth.

You think you have a retirement plan. You don't. You have a concentration risk with a logo.

Let’s talk about why having your entire life’s work tied up in one illiquid asset is a gamble that the house usually wins.

The Piggy Bank That Might Not Open

Most owners treat their business like a giant, ceramic piggy bank.

They assume that when they are tired, or old, or just "done," they can simply crack the thing open and the cash will pour out. They imagine a line of buyers waiting to hand over a check that covers their lifestyle for the next thirty years.

Reality check: The market doesn't owe you a retirement.

Your business is only worth what someone else is willing to pay for it on a Tuesday morning in a bad economy. If you haven't prepared for an exit, that piggy bank is made of reinforced steel, and you don't have the combination.

When your entire net worth is locked inside your four walls, you are one industry shift, one health crisis, or one economic downturn away from losing everything.

The Concentration Trap

Diversification is a boring word used by financial advisors to sell mutual funds. But in the world of Before the Clock Decides, diversification is a survival strategy.

Think about it this way:

- Would you put 90% of your money into a single stock? No.

- Would you bet your entire retirement on a single hand of blackjack? No.

Yet, you do exactly that every single day you operate without a plan to extract value.

Your business is an operating asset, not a savings account.

An operating asset requires constant fuel: your time, your energy, and your capital. A savings account is supposed to be there when the fuel runs out. If the asset and the savings are the same thing, what happens when the engine stalls?

Why "Running It Until I Die" Is a Terrible Strategy

I hear this a lot: "Mike, I love what I do. I’ll just run it until I can’t anymore."

That sounds noble. It’s actually selfish and short-sighted.

If you run the business until you "can't," you are guaranteed to exit at the lowest possible value. Why? Because you’ll be exiting under duress.

Buyers smell blood. If they see an owner who has to sell because of health issues or burnout, the price goes down. The terms get uglier. The valuation you spent twenty years building evaporates in twenty minutes of negotiation.

Your exit is your retirement.

If you don't have a "Plan B": investments, real estate, or cash outside the business: you are a prisoner to your company’s performance. You can’t afford to walk away, which means you’ve stopped being an owner and started being a high-stakes employee of your own creation.

The Buyer’s Perspective: They Don’t Care About Your Needs

Here is a blunt truth: A buyer does not care how much money you need to retire.

They don’t care about your mortgage, your grandkids' college fund, or your dream of buying a boat. They care about Return on Investment (ROI).

If your business is "all-in" on you: meaning you are the primary driver of sales, culture, and operations: the business is worth significantly less to a buyer. They see risk. They see a business that might break the moment you leave.

If your net worth is tied to a business that depends entirely on your heartbeat, you aren't building wealth. You’re building a job that you can’t quit.

Taking Chips Off the Table

You don't have to sell the whole thing tomorrow to start de-risking. You need to start thinking like an investor, not just a founder.

- Stop Reinvesting Every Cent: I know, the business "needs" it. But you need a life outside the business. Start taking a market-rate salary and a distribution that goes into assets you don't control.

- Build a Sellable Asset: Even if you never sell, a "sellable" business is a better business to own. It means it can run without you.

- Audit Your Risk: If your business disappeared tomorrow, what would be left? If the answer is "not much," you are in the danger zone.

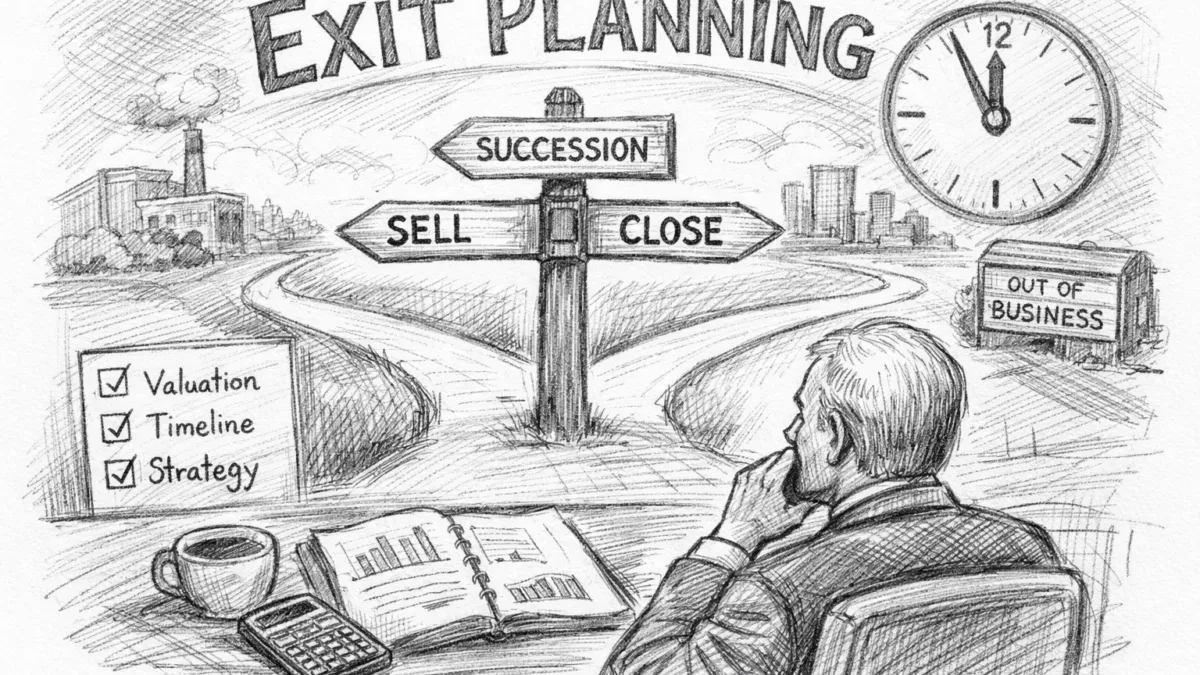

I talk about this extensively in my book. We focus on the "Clock" because time is the only variable you can't negotiate with.

The Diagnostic Questions

Ask yourself these questions. Be honest. There’s no one else in the room.

- If a competitor moved in across the street and cut your revenue by 40% tomorrow, could you still retire?

- What percentage of your monthly income comes from sources other than your business salary or distributions?

- Does your "retirement plan" rely on a specific multiple that a buyer hasn't actually offered you yet?

If these questions make you sweat, good. That’s the feeling of reality hitting your ego. It’s time to move.

The "Plan B" Isn't About Giving Up

Having a backup plan isn't a sign of weakness. It’s a sign of intelligence.

It gives you leverage. The most powerful position in any negotiation is the ability to walk away. If you have 90% of your net worth in the business, you can't walk away. You are a forced seller. And forced sellers get slaughtered.

When you diversify your wealth: when you have "Plan B" assets working for you: you can wait for the right buyer. You can hold out for the right price. You can protect your legacy.

You built this thing from nothing. Don't let a lack of planning turn your greatest achievement into your biggest liability.

Your Move

Don't wait for the market to tell you what your life is worth. Take control of the clock before it decides for you.

- Calculate your "Concentration Score": Divide your business equity by your total net worth. If it’s over 70%, you’re in the red.

- Get an objective valuation: Stop guessing what your business is worth based on "industry standards" or what your buddy sold his for. Get the hard numbers.

- Schedule a strategy session: If you’re ready to stop gambling with your future, let’s talk. You can work with me to build a roadmap that actually leads to freedom.

The clock is ticking. Are you going to watch it, or are you going to wind it?

– Mike Steward