You think you’ve built an asset.

You’ve spent years, maybe decades, sweating the details, making the payroll, and winning the clients. You’re ready to reap the rewards. You want to see that wire transfer hit your account and finally head for the coast.

But when you open the hood for a professional buyer, they don’t see a powerhouse. They see a glass house.

They see fragility.

In my years as a broker and partner at Before the Clock Decides, I’ve watched multi-million dollar deals crumble in forty-eight hours. Not because the revenue wasn't there, but because the risk was too high.

Selling a business isn't about what you’ve done; it’s about what the buyer can do without you.

If your business is built on a foundation of "what-ifs," it isn't an asset. It’s a liability in a tuxedo.

Here are the five hidden risks that make buyers walk away.

1. The "You" Dependency

What happens if you disappear for three months?

If the answer is "the doors close," you don't own a business. You own a high-stress job.

Buyers are not looking to buy your talent. They are looking to buy your systems. They want a machine that prints money regardless of who is turning the crank.

When a buyer sees that you are the primary salesperson, the chief problem solver, and the only one with the "secret sauce" relationships, they see a massive risk. If you leave, the value leaves.

The hard truth: A business that relies on the owner’s charisma is a business that is too fragile to sell.

Buyers want to see standard operating procedures (SOPs). They want to see a management team that makes decisions without texting you first. They want to see a business that survives your exit, not one that mourns it.

If you are the bottleneck, you are the reason your valuation is in the gutter.

2. The Financial "Shoebox"

Messy books are the fastest way to kill trust.

I’ve seen owners try to explain away "personal expenses" run through the business as if it’s a clever tax hack. To a buyer, it’s just a red flag. It tells them your data is unreliable.

If your financial statements are inaccurate or disorganized, a buyer will assume the worst. They won't think, "Oh, they just have a bad bookkeeper." They will think, "What else are they hiding?"

Inaccurate financial records are the number one deal killer.

Buyers want to see:

- Three years of clean, CPA-reviewed or audited statements.

- Clear separation between personal and business expenses.

- Consistency in how you report revenue and costs.

If they have to spend six weeks trying to figure out your true EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), they will simply move on to the next deal. There is always another deal.

Don’t expect a buyer to pay for "potential" that isn't proven on paper. If it’s not in the books, it didn’t happen.

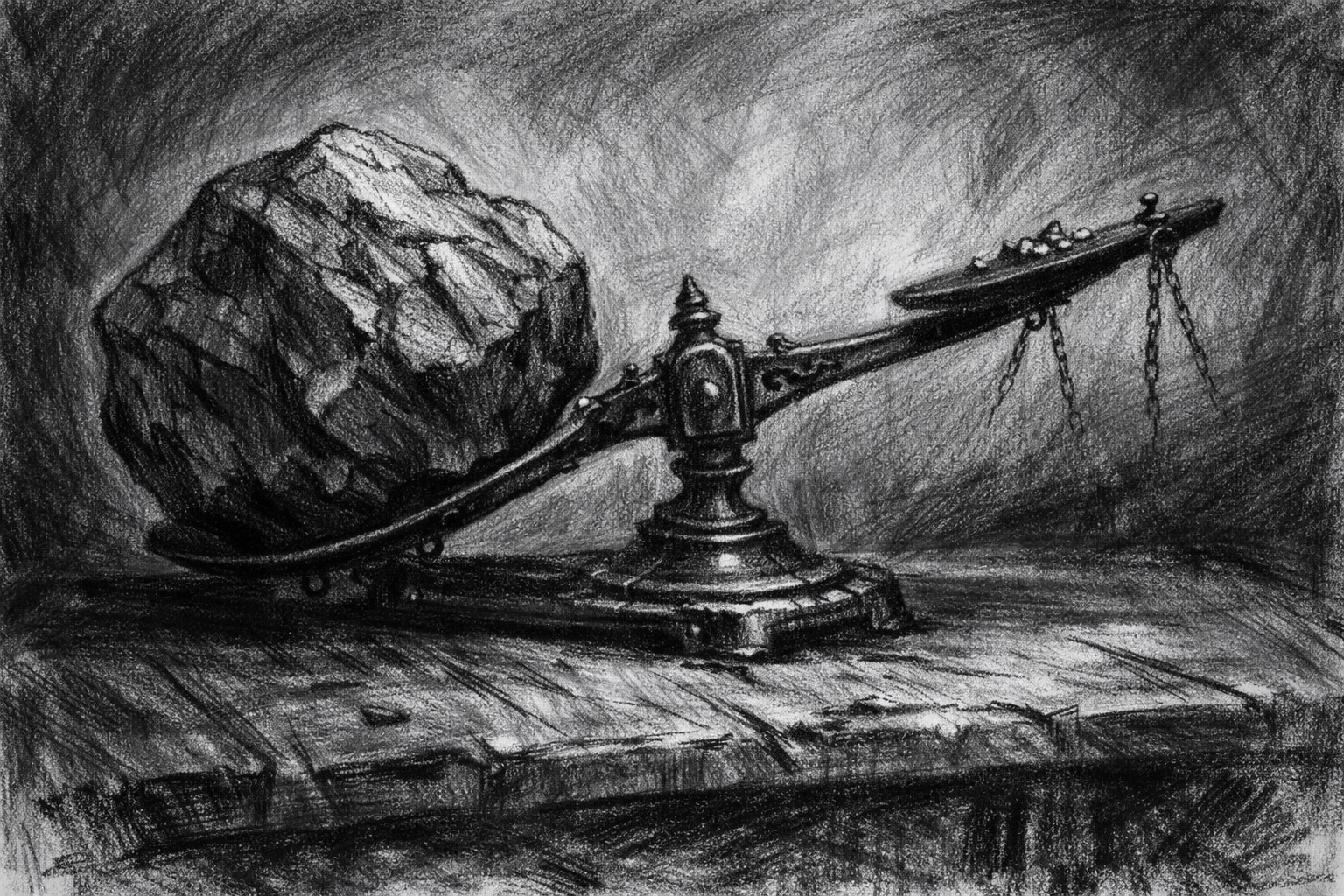

3. Excessive Customer Concentration

You have a $10 million company. That’s great.

But if $3 million of that comes from one single client, your business is one bad mood away from bankruptcy.

This is called customer concentration, and it terrifies buyers. If one customer accounts for more than 20% of your revenue, you are in the danger zone.

The Risk: The buyer knows that once the owner (you) leaves, that big client might use the transition as an excuse to renegotiate or leave.

I’ve seen deals get slashed by 40% in value just because the revenue was too top-heavy. The buyer isn't just buying your profit; they are buying the certainty of that profit.

Visual: A black and white pencil sketch of a scale, with one large heavy stone on one side and several tiny pebbles on the other, symbolizing the imbalance of customer concentration.

If you want a premium price, you need a diverse client base. If your biggest client left tomorrow, would you still be able to pay your staff? If the answer is "no," your business is fragile.

4. The Skeleton Closet: Hidden Liabilities

Due diligence is a colonoscopy for your business.

Buyers will find the skeletons. They will find the disgruntled former employee who wasn't paid overtime. They will find the sales tax you forgot to remit in three states. They will find the "handshake deal" with a vendor that isn't actually in writing.

Hidden liabilities include:

- Unresolved legal disputes: Even if you think it’s "nothing."

- Tax exposure: Especially with the complexity of modern nexus laws.

- Poorly drafted contracts: Agreements that can’t be assigned to a new owner.

- Intellectual property issues: Who actually owns the code or the brand?

If a buyer uncovers a significant liability that you didn't disclose upfront, the trust is gone. Once trust is gone, the deal is dead.

Be honest about your mess before you go to market. It is much easier to sell a business with a known problem than a business with a hidden one.

5. Buyer Paralysis (The Fear Factor)

We often focus on the numbers, but we forget the human across the table.

Many individual buyers are risking their entire life savings. They are taking out SBA loans. They are putting their house on the line.

They are terrified.

If your business feels "fragile", if the systems are loose, the staff is unhappy, or the industry looks volatile, the buyer's fear will paralyze them. They will find a reason to say no.

Your job as a seller is to provide a "sleep at night" asset.

A business is not a product; it is a promise of future cash flow.

If the buyer doesn't believe the promise, they won't sign the check. You need to demonstrate stability, not just growth. You need to show them that the transition will be boring. Boring is safe. Safe is expensive.

Why Preparation Beats Passion

Most owners wait until they are burnt out to sell.

By the time they call me at Before the Clock Decides, they are exhausted. They want out yesterday.

But a burnt-out owner makes mistakes. They neglect the business in the final months, causing revenue to dip. They get impatient during negotiations. They let the "fragility" show.

If you want to walk away with the legacy and the check you deserve, you have to prepare. You have to fix the cracks in the glass before the buyer shows up with a hammer.

You can’t wait for the clock to decide. By then, it’s too late.

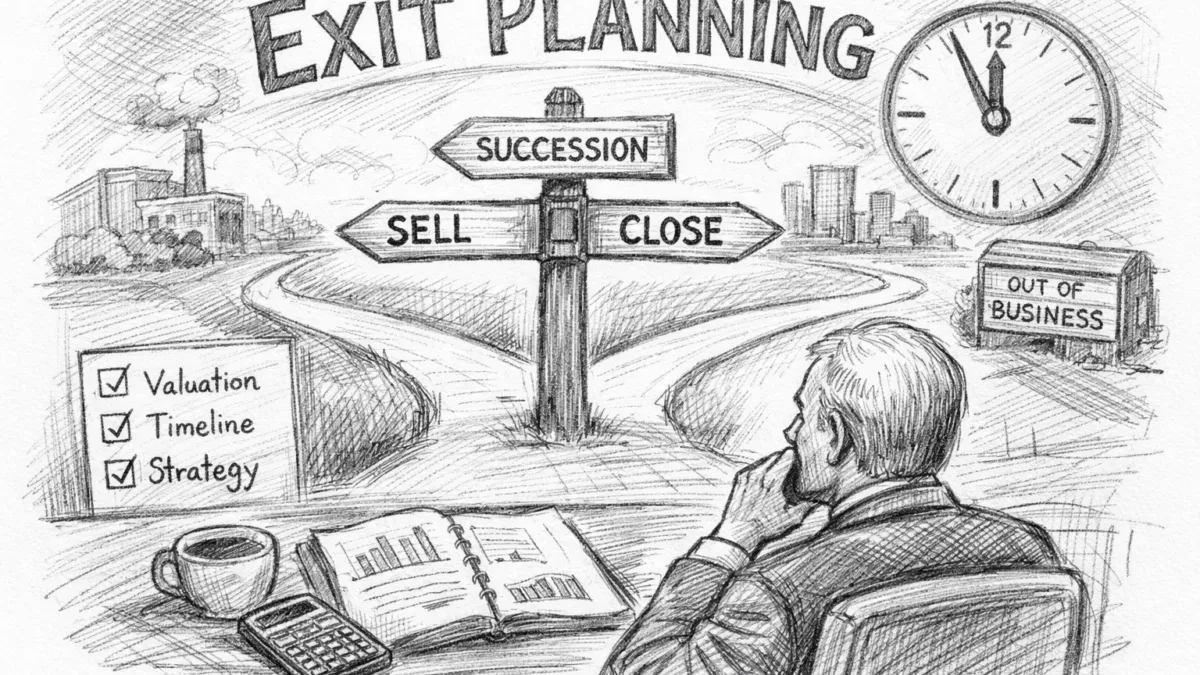

Your Move

Don't wait for a buyer to tell you your business is fragile. Figure it out now while you still have the time to fix it.

- Run the "Disappear Test": Take a two-week vacation without your phone. See what breaks. Fix those things first.

- Audit Your Revenue: Calculate your customer concentration. If any one client is over 15-20%, start a push for new business elsewhere.

- Clean the Books: Hire a professional to look at your financials through a buyer's lens. If you need resources on how to value your business correctly, check out our books and guides.

- Get a Reality Check: If you aren't sure what your business is worth or if it’s even sellable, let’s talk.

The market is honest. It doesn't care about your hard work; it cares about risk.

Make your business unshakeable. Then, and only then, will it be truly sellable.

Mike Steward

Broker, Partner

Before the Clock Decides