You just signed the Letter of Intent (LOI).

The number is big. Your ego is bigger. You’re already picturing the boat or the beach or the early retirement.

Stop.

You haven’t sold anything yet. All you’ve done is given a professional buyer permission to put on the latex gloves and start the "proctology exam" known as due diligence.

If you think this is a routine checkup, you’re in for a violent awakening. Due diligence is not about "confirming" your greatness. It is a systematic attempt to find a reason to pay you less or walk away entirely.

It is invasive. It is exhausting. And if you aren't prepared, it will break you.

The Myth of the "Smooth" Deal

Most owners believe their business is a well-oiled machine.

The reality? Most businesses are a collection of "workarounds" and "tribal knowledge" held together by the owner’s sheer force of will.

Buyers don't care about your will. They care about risk.

Due diligence is the process of peeling back the skin of your company to see if the muscles and bones are actually there. They are looking for "cancer": unpaid taxes, pending lawsuits, key employees ready to quit, or what your business is really worth vs. what you told them it was worth.

The harder you make it for them to find the truth, the more they assume the truth is ugly.

Black and white sketch: A magnifying glass hovering over a mountain of disorganized paperwork.

The Three Pillars of Pain

The exam usually covers three main areas. If you fail any of them, the deal dies.

1. The Financial Colonoscopy

The buyer’s accountants will crawl through your books. They aren't just looking at the P&L. They are looking at the integrity of the data.

- The Trap: "Add-backs." You told the buyer your EBITDA is $2M because you added back your personal car, your vacation to Cabo, and your son’s summer salary.

- The Reality: If you can’t prove those expenses were truly "non-essential" to the business, the buyer will subtract them. Every dollar they "disallow" could cost you $5 or $6 in the final sale price.

2. The Legal Interrogation

Do you actually own what you say you own?

- Contracts: If your "key customer" contract expired three years ago and you’re working on a "handshake," the buyer sees zero value.

- IP: If your nephew wrote the code for your software but never signed an IP assignment, you don’t own your software.

3. The Operational Autopsy

What happens if you disappear?

If the business stops breathing when you take a week off, the buyer isn't buying a company. They are buying a job. And they don't want your job. They want an owner-optional business.

Why Owners Lose Their Minds

The "exam" usually lasts 60 to 90 days. It feels like six years.

The buyer will ask for the same document three times. They will ask questions that feel insulting. They will find a $400 discrepancy in a $10M deal and treat it like a federal crime.

This is intentional.

It’s called "deal fatigue." The buyer wants to wear you down. If you are exhausted, you are more likely to agree to a price "re-trade" (a price drop) in the final hour just to make the pain stop.

The "Hard Truth": Due diligence is 20% math and 80% psychological warfare.

How to Survive Without Losing the Deal

You don’t survive by being "likable." You survive by being prepared.

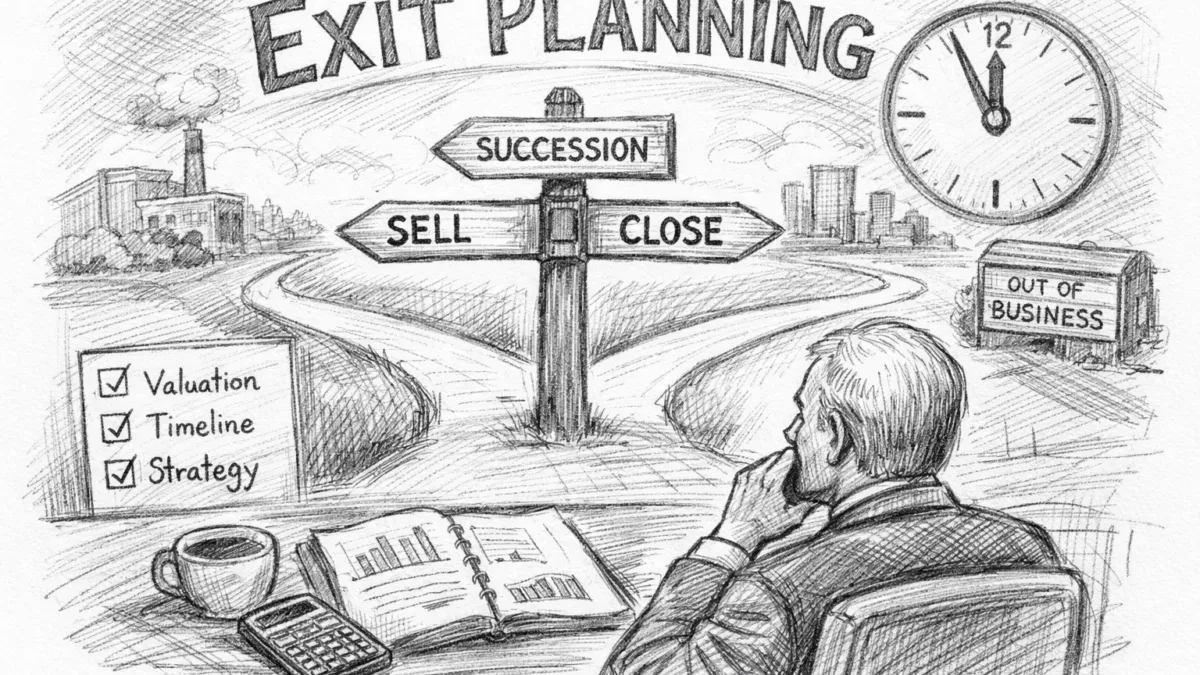

1. Build the "Data Room" Before You Need It

Don't wait for the LOI to start looking for your articles of incorporation. You should have a digital folder ready to go months: even years: before you sell. Exit planning starts earlier than you think.

If a buyer asks for a document and you provide it in 20 minutes, you signal control. If it takes you two weeks, you signal chaos.

2. Run Your Own "Quality of Earnings" (QofE)

Don't let the buyer's accountant be the first person to find the holes in your books. Hire a third-party firm to do a sell-side QofE. It’s expensive. It’s also the best insurance policy you can buy.

It allows you to fix the "red flags" before the buyer ever sees them.

3. Shut Up and Let the Pro Work

Most deals are killed by the owner talking too much.

You feel the need to "explain" or "justify" why things are the way they are. The buyer interprets your "explanation" as "defensiveness."

Your broker or advisor is your buffer. Let them handle the friction. Your job is to keep running the business so the numbers don't dip while you’re distracted.

The "Clean Room" Strategy

Imagine your business is a laboratory.

If the buyer walks in and sees spills on the floor and unorganized equipment, they won't trust the results of your experiments.

Due diligence preparation is about "cleaning the lab."

- Is your cap table clean? (No "phantom" equity promised to old employees).

- Are your employee files complete? (Signed offer letters, I-9s, non-competes).

- Is your tax history boring? (Boring is good. Creative is bad).

If it isn't documented, it doesn't exist. "We've always done it that way" is the most expensive sentence in the English language during a business sale.

The Question That Breaks Most Owners

During the "exam," a smart buyer will eventually ask: "What breaks if you disappear for 90 days?"

If your answer is "Everything," you just lost 30% of your deal value.

The "Proctology Exam" is designed to find the tether between you and the revenue. If the tether is too tight, the buyer will cut the price to compensate for the risk of you leaving.

Black and white sketch: A pair of scissors poised to cut a rope connecting a person to a building.

The Psychological Survival Guide

You will want to quit. You will want to tell the buyer to go to hell. You will feel like they are calling your "baby" ugly.

Remember: It’s not personal. It’s a transaction.

The buyer is putting millions of dollars at risk. They have a fiduciary responsibility to be "pests."

The Moment of Truth: The deal is most likely to fail in the last 10 days of due diligence. This is when the "small" issues aggregate into "big" doubts. Stay calm. Stay detached.

Your Move

The "exam" is coming. You can either be the patient who is surprised by the procedure, or the one who showed up prepared.

- Self-Audit: Spend this weekend looking at your files. If a buyer asked for your top 5 customer contracts right now, could you produce them in 5 minutes?

- Clean the Books: Stop running personal expenses through the business. It makes you look like a hobbyist, not a CEO.

- Identify the Gaps: What is the one "skeleton" in your closet you're hoping they won't find? They will find it. Figure out how to disclose it on your terms before they discover it on theirs.

The clock is ticking. You decide if you're ready for the exam, or if the exam will end your exit.

Need to know if you're actually ready? Check out the most expensive mistake business owners make. Hint: It’s waiting until the "exam" starts to start cleaning the room.