You just had your best year ever.

Revenue is up. Profit is at an all-time high. You feel like a genius. You think this is the perfect moment to hang the "For Sale" sign and walk away with a massive check.

You are probably wrong.

In the world of business exits, one great year is an outlier. To a buyer, it’s a red flag. They don't care about your "best year." They care about what happens the year after they buy you.

They care about Quality of Earnings (QofE).

If you want to sell your business for what it’s actually worth: not just a discounted fraction of your "peak": you need to understand that earnings are not created equal.

The Myth of the Top Line

Most owners think valuation is a simple math problem: Profit times Multiple equals Value.

It isn't.

Value is a measurement of risk. The "Quality of Earnings" analysis is the tool buyers use to find the holes in your story. They aren't looking at what you made; they are looking at how you made it and if it will happen again without you.

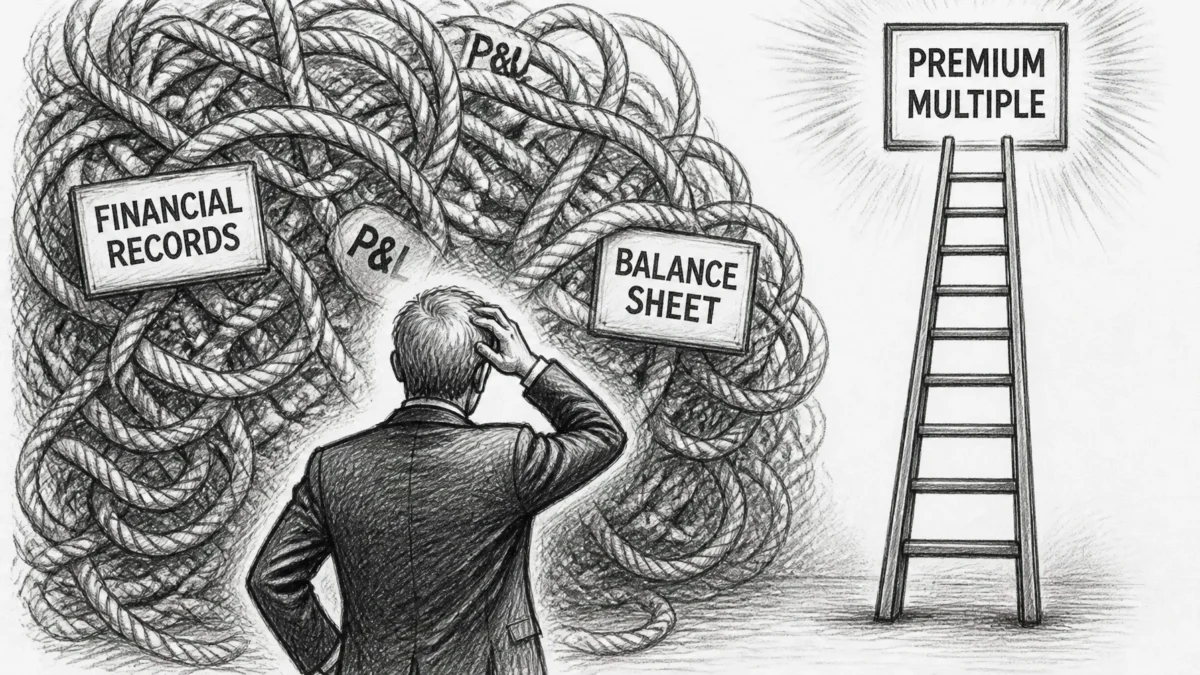

Quality of Earnings is not your P&L.

Quality of Earnings is not your tax return.

Quality of Earnings is not "what's in the bank."

QofE is a deep dive into the sustainability, accuracy, and repeatability of your cash flow. If your record year was driven by a global pandemic, a one-time government contract, or a temporary supply chain fluke, those earnings are "low quality."

To a buyer, those dollars are worth zero.

What Makes a Dollar "High Quality"?

A high-quality dollar is boring. It’s predictable. It’s a dollar that shows up every month because your systems work, not because you caught a lucky break.

Here is the hierarchy of earnings quality:

- Repeatability: Does the revenue come from recurring contracts or a diversified base of loyal customers?

- Predictability: Can you forecast next quarter with 90% accuracy?

- Transferability: If you leave tomorrow, does the money stay?

- Cash Conversion: Is the profit actually sitting in the bank, or is it stuck in accounts receivable that may never be collected?

If your earnings rely on your personal relationships or a single "hero" employee, your quality of earnings is low. If 40% of your revenue comes from one client, your quality of earnings is dangerous.

The buyer is buying your future, not your past.

If they can’t see a clear path to repeating your "best year," they will price your business based on your "worst year."

Why One Year Isn't a Trend

A single year is a snapshot. Three years is a story.

Buyers look for a three-year lookback for a reason. They want to see the trajectory.

- Is the business growing because the market is lifting all boats?

- Did you slash marketing and maintenance just to "fatten the pig" before the sale?

- Are your margins expanding because of efficiency or because you haven't raised wages in five years?

If you spike the ball in year three after two years of flat performance, the buyer will normalize your earnings.

"Normalization" is a polite way of saying they are going to strip out your record year and replace it with an average. They will find every one-time gain and delete it. They will find every under-market expense and add it back.

By the time they are done, that "record profit" you were counting on might look a lot smaller.

The Diagnostic: What Breaks If You Disappear?

Ask yourself these questions. Be honest. The market will be.

- Who owns the key relationships? If it’s you, the earnings are low quality.

- What happens if your top customer leaves? If the business dies, the earnings are low quality.

- Is your accounting "creative"? If you’re running your personal life through the business, the buyer will find it, and they will trust nothing else you say.

- Are your systems documented? If the "way we do things" is all in your head, the earnings are low quality.

A Quality of Earnings report is often the difference between a deal that closes and a deal that falls apart in due diligence.

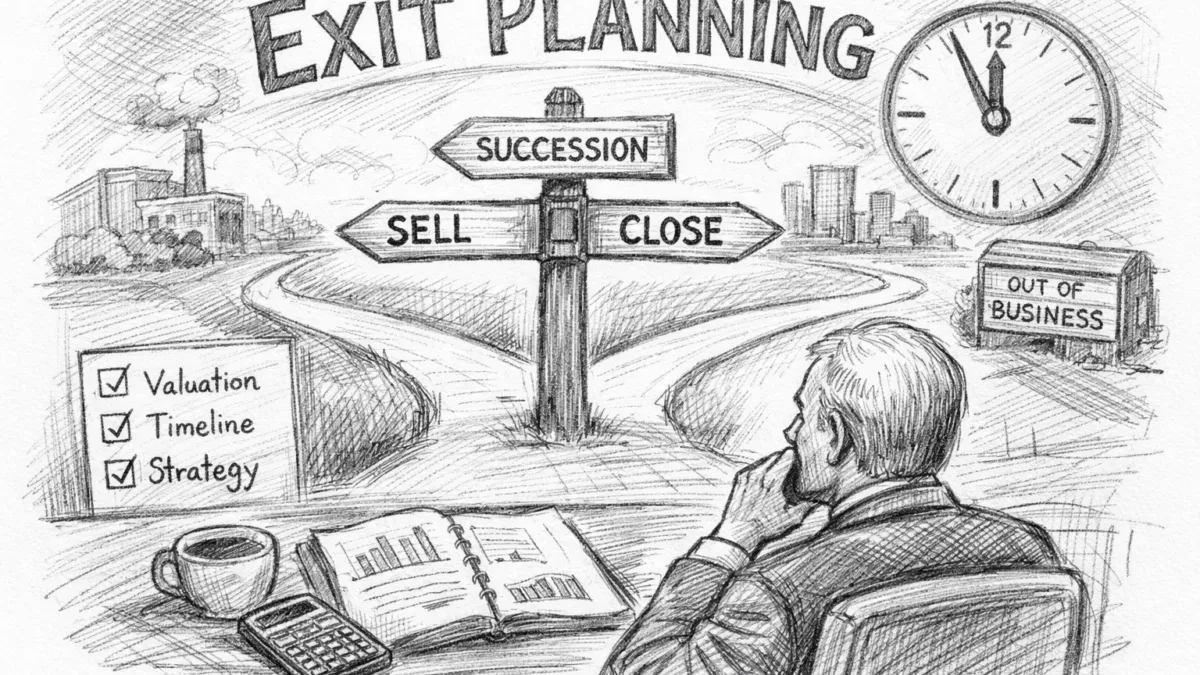

Why You Should Do Your Own QofE First

Most owners wait for the buyer to perform a QofE analysis. This is a mistake.

When the buyer does the analysis, they are looking for reasons to drop the price. They are looking for "gotchas."

When you perform a Sell-Side Quality of Earnings report before you go to market, you are taking control of the narrative. You find the skeletons in the closet before the buyer does. You fix the accounting errors. You explain the one-time expenses.

You show the buyer that you aren't just a "lucky" owner who had a good year: you are a professional who runs a high-performance machine.

If you don't know your numbers, you don't own your exit.

You can find more resources on preparing your business for this level of scrutiny in our Free Resources section.

The Harsh Reality of the Market

The market does not care how hard you worked. It does not care that you sacrificed weekends for a decade. It does not care about your "potential."

The market cares about risk-adjusted cash flow.

If your business is a "black box" where money goes in and out but no one is sure why, the buyer will walk. Or worse, they will offer you a "structure" deal: an earn-out where you only get paid if the business continues to perform after you leave.

An earn-out is the buyer’s way of making you prove your earnings were high quality.

If you want the cash upfront, you have to prove the quality before you sign the Letter of Intent (LOI).

One great year is a start. It’s a reason to have a conversation. But it is not a reason to write a check. Stability, systems, and transparency are what drive multiples.

If you're still relying on a "gut feeling" about what your business is worth, you're playing a dangerous game. You need to see the business through the eyes of a buyer before the clock decides your fate.

You can check out my book, Before the Clock Decides, for a deeper dive into how to build a business that actually sells.

Your Move

You cannot fix your Quality of Earnings in a week. You cannot "audit" your way into a higher valuation thirty days before a sale.

1. Clean the Books: Stop running personal expenses through the business. Immediately.

2. Diversify: If one customer is more than 15% of your revenue, start hunting for new ones today.

3. Document the Machine: Turn your "expertise" into a manual. If a stranger can't run the process, it isn't an asset; it’s a job.

4. Get a Sell-Side QofE: Don't wait for the buyer to tell you your business is worth less than you thought. Find out now while you still have time to fix it.

The clock is ticking. Every day you operate without a clear understanding of your earnings quality is a day you are gambling with your net worth.

Stop focusing on having a "great year" and start focusing on building a "great company."

The price tag will follow.

Need a guide to navigate the exit process? Work with Mike and ensure you aren't leaving money on the table when it’s time to walk away.