You think you’ve won.

The Letter of Intent is signed. The number on the page looks like a telephone number. You’re already picturing the boat, the beach, or the quiet mornings without an inbox full of fires to put out.

But then you see the "structure."

$10 million total. $6 million at closing. $4 million in an earnout over three years.

You tell yourself it’s fine. You’re a high-performer. You’ve hit your targets for a decade. Why wouldn't you hit them now?

Here is the truth you won't hear from the buyer: An earnout is not a bonus. It is a debt the buyer hopes they never have to pay.

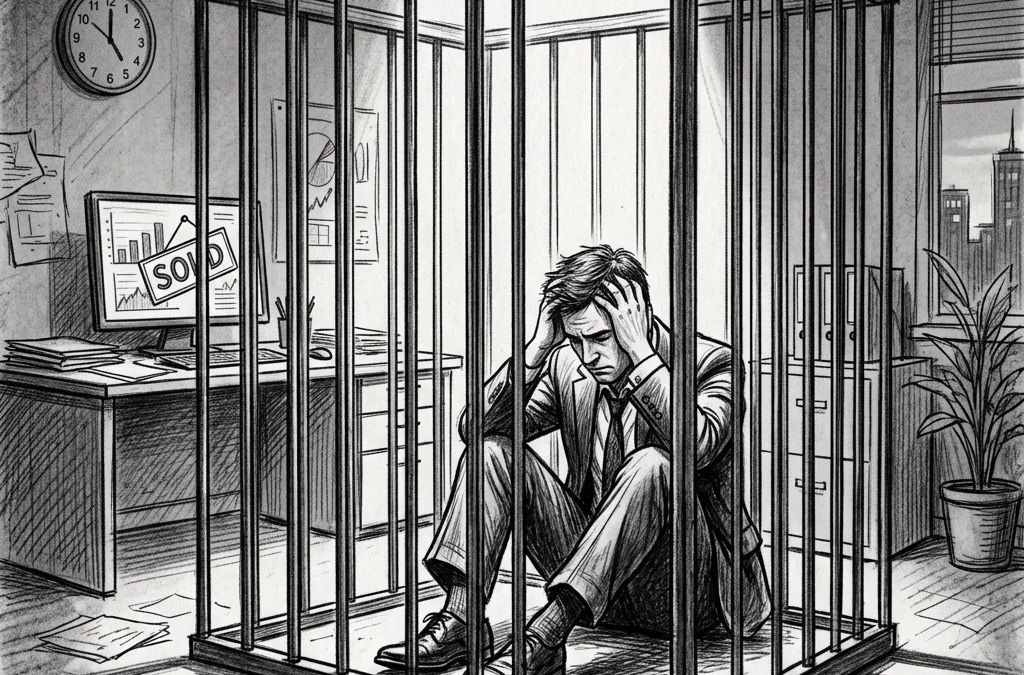

If you don’t understand how to bridge the gap between "sold" and "free," you’ll end up as a glorified employee in a company you used to own, watching your payout evaporate while you do all the heavy lifting.

What an Earnout Is Not

Before we talk about how to win, let’s define what we’re actually dealing with.

An earnout is not a victory lap.

An earnout is not a guaranteed payment.

An earnout is not a sign that the buyer trusts you.

In reality, an earnout is a tool used to bridge a valuation gap. The buyer thinks your business is worth $6 million. You think it’s worth $10 million. The earnout is the "prove it" clause.

It is a shifting of risk from the buyer’s shoulders onto yours. If the market dips, you lose. If the buyer integrates poorly, you lose. If the buyer changes the strategy, you lose.

The Illusion of Control

The moment the ink dries on the purchase agreement, the power dynamic shifts.

You are no longer the captain. You are a consultant. Or worse, a middle manager.

You might have a target based on EBITDA or Revenue. But who controls the expenses now? The buyer.

If the buyer decides to hire six new expensive VPs and "allocate" those costs to your P&L, your EBITDA vanishes. So does your earnout.

If the buyer decides to pivot the sales team to a different product line, your revenue target becomes an impossible mountain.

The Trap: You feel responsible for the numbers, but you no longer have the authority to move them.

The Leverage Window: It’s Shorter Than You Think

Most founders wait too long to negotiate the earnout protections.

They wait until the "definitive legal documents" phase. By then, it’s over.

Your leverage is at its absolute peak the moment before you sign the Letter of Intent (LOI). Once that LOI is signed, you are in "exclusivity." You can’t talk to other buyers. Your leverage drops to near zero.

If you haven't defined the earnout protections in the LOI, you are walking into a knife fight with a toothpick.

I've seen it happen dozens of times. A founder signs an LOI with a vague earnout. Two months later, during due diligence, the buyer starts adding "adjustments" and "limitations." The founder feels trapped because they’ve already told their spouse and their board that the deal is happening.

They sign anyway. They regret it for three years.

The Three Pillars of Earnout Protection

If you want to avoid the "trapped" feeling, you need to bake these three things into your deal before you commit.

1. The "Termination Without Cause" Shield

This is the most common way earnouts die.

The buyer acquires you. Six months later, they realize they don't actually need you to run the day-to-day. They fire you "without cause."

In a standard, unprotected contract, your earnout rights die with your employment. The buyer just saved $4 million by handing you a pink slip.

The Hard Truth: If your presence is required to hit the targets, you must negotiate for an "Acceleration Clause." If they fire you without cause, the earnout should be considered fully earned and paid out immediately.

If they won't agree to that, they are planning to fire you. Believe them.

2. Guarding the "Key Players"

You aren't the only one who hits the targets. Your lead dev, your head of sales, and your operations manager are the ones doing the work.

If the buyer moves in and makes life miserable for your key staff, and they quit, you will miss your targets.

You need to negotiate for the right to maintain staffing levels or, at the very least, ensure that the departure of key personnel (due to the buyer's actions) triggers a adjustment in the earnout targets.

3. Auditable, Transparent Metrics

Never agree to an earnout based on "Net Income."

Net Income is a fairy tale written by the buyer’s accountants. It includes taxes, interest, and corporate overhead allocations that you cannot control.

If the buyer decides the "corporate headquarters" needs a new private jet, and they allocate a portion of that cost to your business unit, your Net Income takes a hit.

The Strategy: Stick to Top-Line Revenue or Gross Margin. These are harder to manipulate. If you must use EBITDA, you need a strict list of "add-backs" and a prohibition on corporate overhead allocations.

The Psychological Cost of the "Golden Handcuffs"

We talk a lot about the money. We don't talk enough about the mental health.

Selling a business is an emotional divorce. You are handing over your "baby" to someone else.

If you are under an earnout, you have to watch that person "parent" your baby poorly. They will make mistakes. They will change the culture. They will ignore your advice.

If you don't have a clear earnout structure, every mistake they make feels like they are reaching into your pocket and stealing your money. It leads to resentment, burnout, and litigation.

I wrote about this transition in my book, Before the Clock Decides. The transition isn't just financial; it's identity-based. If you are still tied to the financial performance but have no power, you will feel like a prisoner in your own office.

Diagnostic Questions: Are You Setting a Trap?

Before you agree to that earnout, ask yourself these questions:

- What breaks if I disappear tomorrow? If the answer is "everything," and the earnout requires you to stay, you are high-risk.

- Can the buyer hit these targets without my help? If no, why are they making the payment contingent?

- Do I trust the buyer's CFO more than my own? Because after the deal, the buyer's CFO is the one who signs the checks.

- Is the "Cash at Closing" enough to make me happy if I never see a dime of the earnout?

If the answer to that last question is "No," walk away from the deal.

An earnout should be the cherry on top, not the sundae. If you need the earnout to feel like you got a fair price, you haven't sold your business: you've taken a high-stakes bet with a house that owns the cards.

The "Negative Definition" of a Good Deal

A good deal isn't one where you get the highest possible number.

A good deal is one where you don't have to sue the buyer three years later.

A good deal is one where you aren't checking the P&L at 2:00 AM in a cold sweat.

A good deal is one where the "trapped" feeling never has a chance to take root.

At Before the Clock Decides, we focus on intentional transitions. That means looking past the big number and looking at the "Day 2" reality.

If you want to see how other founders have navigated these waters, check out our book reviews or reach out to Mike Steward directly.

Your Move

Don't let the excitement of an exit blind you to the reality of the structure.

- Audit your current LOI. Does it specify what happens to your earnout if you are terminated without cause?

- Define your metrics. Move from "Net Profit" to "Revenue" or "Gross Profit."

- Set a floor. Negotiate for a higher "Cash at Closing" amount, even if it means a lower total "Potential" price.

The clock is ticking. You can decide how you exit now, or you can let the buyer's contract decide for you later.

Choose wisely.